What we’re seeing in 2022 so far

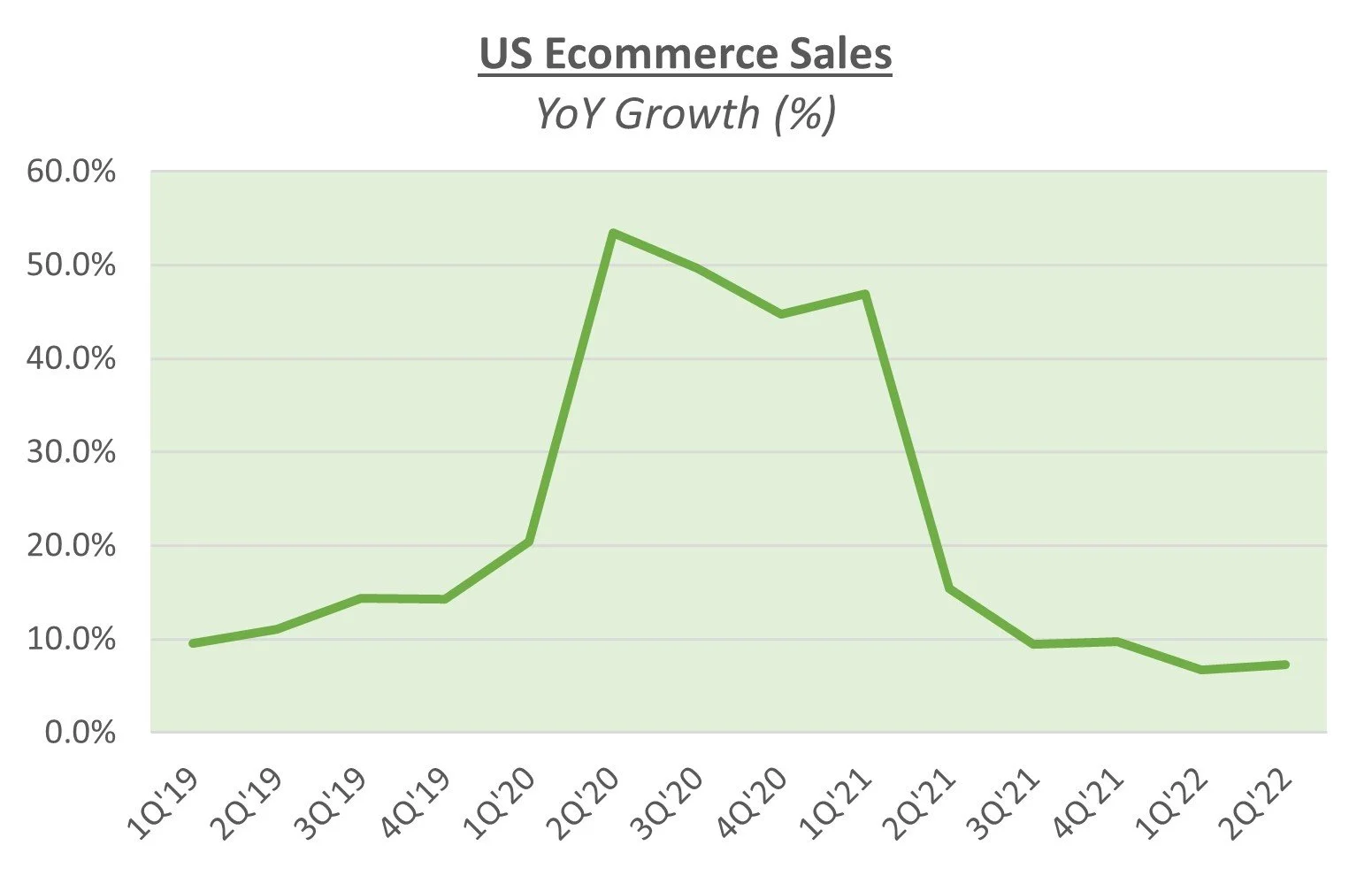

Ecommerce growth has reverted to pre-pandemic levels

After accelerated growth in 2020 and the slow-down in early 2021, US ecommerce growth has reverted to the long-term historical pre-pandemic “normal”.

Source: US Census Bureau

Amazon 3P merchants have led the way

The broader trend is reflected in Amazon’s and Shopify’s GMV growth.

Source: Company public filings; Morgan Stanley Research

There was a notable pickup in Amazon’s 3P business in Q2 (vs the prior two quarters), which was in contrast to a decline in Amazon’s 1P business.

Source: Company public filings; Morgan Stanley Research

Market consolidation continues

Sizeable “household” names in the ecommerce operations space have been acquired, pointing to functional and also customer base expansion amongst key players.

Source: Public Filings, Capital IQ. Estimates as of 9/13/2022

Valuation multiples have returned to historical norms

Source: Capital IQ, BVP SaaS Index. Market data as of 9/13/2022

¹ Bessemer Venture Partners SaaS Index of 75 companies

² Ecom Index composed of 10 ecommerce-centric SaaS companies (BIGC, ECOM, EVCM, FRSH, GDDY, CRM, SHOP, SQSP, WIX, ZUO)

Strong correlation between SaaS company valuation and Rule-of-40

Over a 10-year period, there are clear correlations between valuation bands and median Rule-of-40 (Revenue growth % + EBITDA margin %)metrics:

1-2x EV/ Rev: 11% Ro40

2-3x EV/Rev: 22% Ro40

3-4x EV/Rev: 29% Ro40

4-5x EV/Rev: 33% Ro40

5-6x EV/Rev: 34% Ro40

6-7x EV/Rev: 46% Ro40

Source: Capital IQ, BVP SaaS Index. Market data as of 9/13/2022